Yarab A |Updated on: April 25, 2023

GSTR-3B is a self -assessed monthly return in which the summary of inward and outward supplies needs to be declared by the businesses. However, the invoice-wise details in Form GSTR-1, are required to be filed either quarterly or monthly.

In this blog, let us understand how to fill Form GSTR-3B.

If you are using TallyPrime, you can skip the rest of this blog post. Our new release to supporting Form GSTR-3B is available now - Download.

Form GSTR-3B consists of 6 Tables. You need to capture the consolidated details of outward supplies, inward supplies, eligible ITC, and the details of tax payment. Let us discuss this in detail:

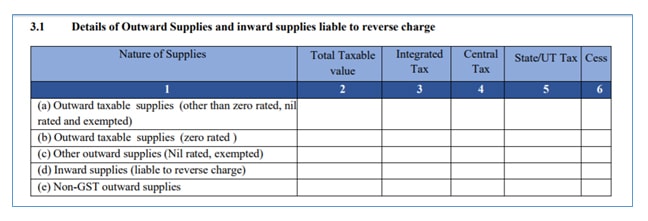

Details of outward supplies and inward supplies liable to reverse charge

In the above table (3.1), you need to capture the total taxable value (both intrastate and interstate) of the following Nature of Supplies along with the total tax (IGST, CGST, SGST/UTGST) as applicable:

- Outward Taxable Supplies other Zero Rate, Nil Rate and Exempted

- Outward Taxable Supplies (Zero Rated)

- Outward Supplies towards Nil Rated and Exempted

- Inward Supplies liable to be paid on reverse charge basis

- Non-GST Outward Supplies

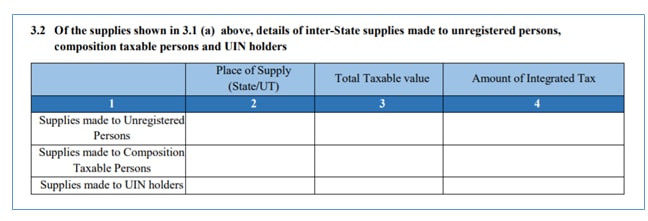

Details of inter-State supplies made to unregistered persons, composition dealer and UIN holders

From the outward supplies details declared in table 3.1, discussed in point No. 1, you need give a break-up of the interstate outward supplies made to Unregistered Persons, Composition Dealers and UIN Holders. These details needs to be captured State-wise/ Union-Territory-wise total with taxable value and total IGST levied on these supplies.

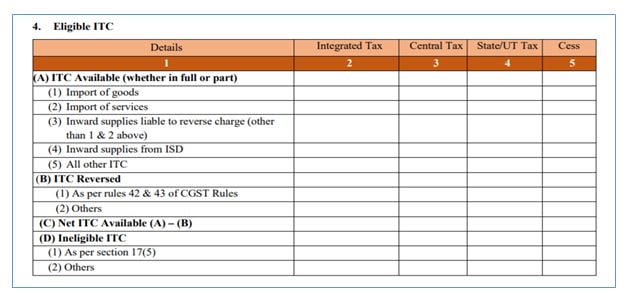

Details of eligible Input Tax Credit

In the above table, you need to capture the details of ITC availability, ITC to be reversed, and arrive at the Net ITC available. The following are the details you need to capture:

- ITC Available (Whether in Full or Part)

You need to give the break-up of inward supplies on which the ITC was availed. The following are the details you need to capture:- Import of Goods: Tax credit of IGST paid on import of goods.

- Import of Service: Tax credit of IGST paid on import of services.

- Inward supplies liable to reverse charge: You need to capture the ITC of GST paid on inward supplies liable for reverse charge such as, sponsorship services, purchase from URD, and so on, other than import of goods or services. To know more, read inward supplies liable to reverse charge

- Inward Supplies from ISD: Input tax credit received from Input Service Distributor (ISD). Read our blog post on ISD for more details.

- All other ITC: Apart from above, ITC of other inward supplies has to be captured here.

- Details of Input Tax credit to be reversed: Under this table, you need to capture the ITC reversible on usage of inputs/input services/capital goods used for non-business purpose, or partly used for exempt supplies. Also, if the depreciation is claimed on tax component of capital goods, and plant & machinery, then the ITC will not be allowed. Such reversal needs to be captured in this table. To know more, read ITC on inputs/input services used for non-business purpose or exempt supplies

The ITC available as reported in Table 4(a) needs to be reduced by the amount of ITC to be revered as reported in above table. The balance will be your eligible ITC.

- Details of Ineligible ITC: GST paid on inward supplies listed in negative list will not be eligible as input tax credit. The details of GST paid on such supplies needs to be recorded in this table. To know more, see the list of supplies ineligible for ITC.

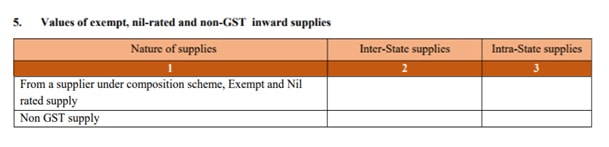

Details of exempt, nil-rated and non-GST inward supplies

You need to capture the details of inward supplies made from the composition dealer, inward supplies at nil rate and exempt. Also, you need to separately mention Non-GST inward supplies. The value of above discussed supplies need to be captured separately for interstate and intrastate supplies.

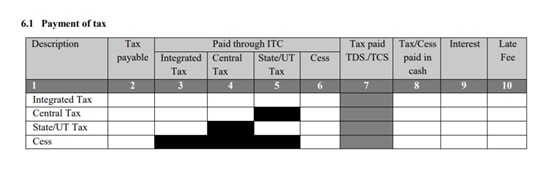

Payment of tax

In the above table (6.1), you need to declare the self-ascertained tax payable. This is based on the details of outward supplies and inwards supplies liable to be paid on reverse charge captured in Table No. 3.1. The tax-wise break-up of payment tax by way of utilization of ITC and cash deposit needs to be provided.

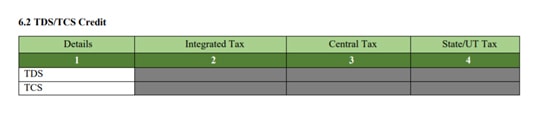

TDS/TCS Credit

In the above table, you need to capture the details of TDS (Tax withheld by the Government establishment) and TCS (Tax withheld by E-commerce operator). However, these provisions are deferred from initial rollout of GST. Accordingly, TDS and TCS is not applicable till it is notified further.

Note: The Value of Taxable Supplies refers to Net Taxable value and formula to calculate is given below:

Taxable value = Value of invoices + value of Debit Notes – value of credit notes + value of advances received for which invoices have not been issued in the same month – value of advances adjusted against invoices.

Latest Blogs

How to Easily Shift/Migrate Your Data to TallyPrime

Nuts & Bolts of Tally Filesystem: RangeTree

A Comprehensive Guide to UDYAM Payment Rules

UDYAM MSME Registration: Financial Boon for Small Businesses

Understanding UDYAM Registration: A Comprehensive Guide

MSME Payment Rule Changes from 1st April 2024: A Quick Guide