Tally Solutions |Updated on: August 24, 2021

Taxation laws have laid down the taxes applicable on import and export of goods and services. In the current tax regime, laws of Customs duty, Excise, Service Tax and VAT lay down the tax treatment of imports and exports. In the GST regime, Excise, Service Tax and VAT will be subsumed into GST and customs duty will continue to be levied separately. Let us understand the tax implication on imports and exports under GST in comparison to the current regime.

Current Regime

Taxes on Import of Goods

In the current regime, a person who imports goods has to pay customs duty, countervailing duty (CVD), and special additional duty (SAD). CVD is levied at a rate equivalent to the rate of Excise on such goods, if they had been manufactured in India. SAD is equivalent to VAT on the goods in India. CVD and SAD are imposed to bring the imported product’s price to its true market price in India. If the importer uses the imported goods to manufacture dutiable goods in India or provide taxable services, CVD paid on inputs is available as tax credit. If the importer is just a trader, CVD on imports is not available as credit. SAD paid on import is eligible for refund, subject to conditions. However, no credit is given on customs duty paid and it becomes a cost for the importer.

Let us see an example to understand the levy of import duties in case of import of goods in the current regime.

Example: Manoj Apparel in Bangalore, Karnataka purchases apparel from a supplier, Oz Designs, in Sydney, Australia.

Tax calculation

| Particulars | Nos. | Price per no. (Rs.) | Amount(Rs.) |

|---|---|---|---|

| Women’s T-shirts | 200 | 2,500 (51.68 AUD) * | 5,00,000 |

| Men’s T-shirts | 100 | 5,000 (103.37 AUD) * | 5,00,000 |

| Total | 300 | - | 10,00,000 |

| Customs duty @ 10% | 1,00,000 | ||

| Customs education cess @ 3% on customs duty (1,00,000*3%) | 3,000 | ||

| Sub total | 11, 03,000 | ||

| CVD @ 12.5% | 1,37,875 | ||

| Sub total | 12,40,875 | ||

| SAD @ 4% | 49,635 | ||

| Total cost of import | 12,90,510 |

* Exchange rate taken is 0.021 AUD = 1 Rupee

Taxes on Import of Services

A person who imports services has to pay Service Tax on the imported service at the Service tax rate applicable in India. The importer can claim tax credit of the Service Tax paid on imports.

For example: Rajesh Apparels in Hyderabad, Telengana, avails fashion designing services of Rs. 50,00,000 from Kaushi Designs in Colombo, Sri Lanka.

Tax calculation

| Particulars | Amount (Rs.) |

|---|---|

| Fashion designing services | 50,00,000 |

| Service Tax @14% | 7,00,000 |

| Krishi Kalyan Cess @0.5% | 25,000 |

| Swachh Bharat Cess @0.5% | 25,000 |

| Total cost of import | 57,50,000 |

Exports

In the current regime, export of goods and services is zero rated, i.e. rate of tax on exports is 0%. An exporter can also claim refund of the tax paid on inputs used to manufacture/purchase/provide the exported goods or services.

GST Regime

GST on Import of Goods

In the GST regime, a person who imports goods has to pay customs duty and IGST. The difference here is that CVD and SAD levied on imports in the current regime will be replaced by IGST under GST. IGST will be levied at the rate applicable to the imported goods in India. An importer can claim full tax credit of IGST paid on imports. Hence, importers who were unable to claim credit of CVD or SAD in the current regime can now claim full tax credit of the IGST paid on imports. However, no tax credit will be given on customs duty paid and it remains a cost for the importer under GST also.

Let us take an example to understand the levy of import duties in case of import of goods in the GST regime.

Example: Manoj Apparel in Bangalore, Karnataka purchases apparel from a supplier, Oz Designs, in Sydney, Australia.

Tax calculation

| Particulars | Nos. | Price per no. (Rs.) | Total Price (Rs.) |

|---|---|---|---|

| Women’s T-shirts | 200 | 2,500 (51.68 AUD) * | 5,00,000 |

| Men’s T-shirts | 100 | 5,000 (103.37 AUD) * | 5,00,000 |

| Total | 300 | - | 10,00,000 |

| Customs duty @ 10% | 1,00,000 | ||

| Education cess @ 3% on customs duty (10,000*3%) | 3,000 | ||

| Sub total | 11,03,000 | ||

| IGST @18% ** | 1,98,540 | ||

| Total cost of import | 13,01,540 |

* Exchange rate taken is 0.021 AUD = 1 Rupee

**Assuming GST rate of 18% on apparel.

GST on Import of Services

Under GST, a supply will be considered as an import of service when-

- The supplier of the service is located outside India.

- The recipient of the service is located in India and

- The place of supply of the service is in India.

For example: Rajesh Apparels in Hyderabad, Telengana, avails fashion designing services of INR 50,00,000 from Kaushi Designs in Colombo, Sri Lanka

Location of supplier: Colombo, Sri Lanka

Location of recipient: Hyderabad, Telengana

Place of supply: Place of supply will be the location of the recipient, i.e. Hyderabad, Telengana.

Hence, this supply is an import.

Tax calculation

| Particulars | Amount (Rs.) |

|---|---|

| Fashion designing services | 50,00,000 |

| IGST @ 18%* | 9,00,000 |

| Total cost of import | 59,00,000 |

* Assuming GST rate of 18% on fashion designing services

GST on Exports

Under GST, exports will be zero rated, similar to the current regime. An exporter can also claim refund of the tax paid on inputs used to manufacture/purchase/provide the exported goods or services.

Export of services

Specific conditions have been laid down for a supply to be considered an export of service under GST. These are:

- The supplier of the service is located in India.

- The recipient of the service is located outside India.

- The place of supply of the service is outside India

- The payment for the service has been received by the supplier in convertible foreign exchange and

- The supplier and recipient are not establishments of the same person.

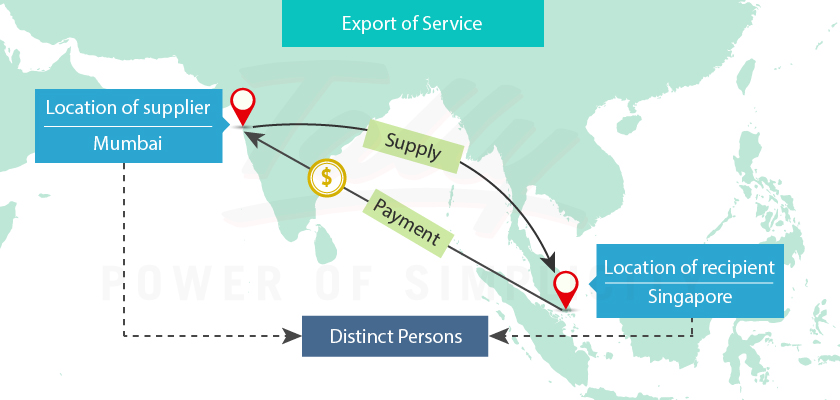

For example: Rohan Consultants in Mumbai, Maharashtra, provides business consultancy services to Abey’s Engineering in Singapore. The payment for the service has been received in Singapore Dollars.

Here,

Location of supplier: Mumbai, Maharashtra

Location of recipient: Singapore

Place of supply: Place of supply will be the location of the recipient, i.e. Singapore.

Payment for the service: Payment for the service has been received in convertible foreign exchange, i.e. Singapore Dollars.

Relationship between the supplier and recipient: The supplier and recipient are not establishments of the same person.

Hence, this supply qualifies as an export of service. Rate of tax on the supply will be 0%.

The levy of taxes and treatment of taxes in case of imports and exports largely remain the same under GST in comparison with the existing laws. In case of an importer, full input credit will be available on the IGST paid on imports and additional input credit will be available on the GST paid on all types of inputs used or intended to be used in the course of or for the furtherance of business. Similarly, in the case of an exporter, refund will be given on the tax paid on all inputs used in the course of business. Overall, costs of import and export are expected to reduce under GST and compliance is expected to become easier with the convergence of multiple tax laws into one law.

Latest Blogs

How to Easily Shift/Migrate Your Data to TallyPrime

Nuts & Bolts of Tally Filesystem: RangeTree

A Comprehensive Guide to UDYAM Payment Rules

UDYAM MSME Registration: Financial Boon for Small Businesses

Understanding UDYAM Registration: A Comprehensive Guide

MSME Payment Rule Changes from 1st April 2024: A Quick Guide