Yarab A |Updated on: March 19, 2021

In the erstwhile tax structure, the taxable events were different for different tax type. The taxable events in the earlier indirect tax structure are given below:

| Type of Tax | Taxable Event |

|---|---|

| Central Excise | Removal of excisable goods |

| VAT | On sale of goods |

| Service Tax | Provision of taxable services |

Taxable event under GST

The taxable event under GST is the Supply of Goods and/Services. All taxes such as Central Excise, Service Tax and VAT/CST will be subsumed under GST, and the concept of manufacture of goods, sale of goods, and provision of services would no longer be relevant.

Thus, for every business, it is crucial to understand the relevance of supply which sets the scope of transactions liable for the levy of GST.

Relevance of supply under GST

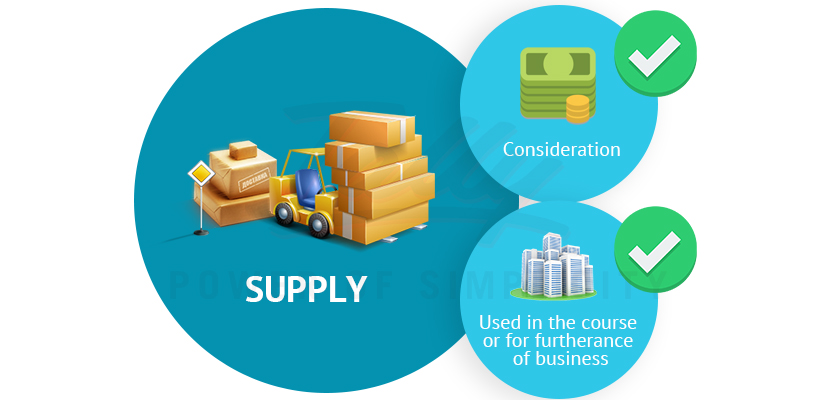

The term 'supply' includes all forms of supply of goods or services, supplied or to be supplied, for a consideration, in the course of or for furtherance of business.

However, there are specific types of supplies mentioned in the law which need to be considered as supply even without a consideration.

Let us understand by categorising the different types of supply as;

- Supplies made for a consideration in the course of or for furtherance of business

- Supplies without consideration

- Supplies made for a consideration whether or not in the course of or for furtherance of business

Supplies made for a consideration in the course of or for furtherance of business

The following are considered as supply with consideration:

|

Any sale of goods or services which broadly result in the transfer of title in case of goods, and transfer of right to use in case of services. |

|

Any transfers between branches form a part of supply and are taxable. However, GST paid on branch transfers are fully available as Input Tax Credit. |

|

When the consideration is paid through goods instead of money. For example: a seller has supplied goods and the buyer, supplies goods to the extent of payment. Or when one product is exchanged with another product. |

|

Any grant of license to use forms part of supply. For example: online subscriptions |

|

Renting of property fully or partially is a supply under GST |

|

Letting out the building or property on lease is a supply under GST |

|

Disposal of business assets forms part of supply |

Latest Blogs

Nuts & Bolts of Tally Filesystem: RangeTree

A Comprehensive Guide to UDYAM Payment Rules

UDYAM MSME Registration: Financial Boon for Small Businesses

Understanding UDYAM Registration: A Comprehensive Guide

MSME Payment Rule Changes from 1st April 2024: A Quick Guide

Are Your Suppliers Registered Under MSME (UDYAM)?