Tally Solutions |Updated on: March 14, 2022

- Introduction to credit note in GST

- What is Credit Note in GST?

- When is a credit note in GST issued?

- Conditions which must be satisfied for issuance of credit note in GST

- Credit note format in GST

- Impact of credit note in GSTR 3B and other monthly returns

Introduction to credit note in GST

To begin with, one must fully unlearn the practices under the erstwhile law in order to clearly understand the concepts of credit note in GST. A credit note in GST can be issued by the registered person who has issued a tax invoice, i.e., the supplier.

What is Credit Note in GST?

A Tax Credit Note is a written or electronic document to be recorded and issued by a registered supplier of goods or services on the occurrence of situations as prescribed by the GST Act and Rules.

When is a credit note in GST issued?

The GST Law provides an exhaustive list of situations under which the registered supplier is entitled to issue a credit note: Following are the situations which requires the supplier to issue a credit note.

- Actual value of supply is lower than that stated in the original tax invoice.

- Tax charged in the original tax invoice is higher than that applicable on the supply.

- Goods supplied are returned by the recipient.

- Goods or services supplied are deficient.

Examples of Credit Note

Example -1 of Credit Note

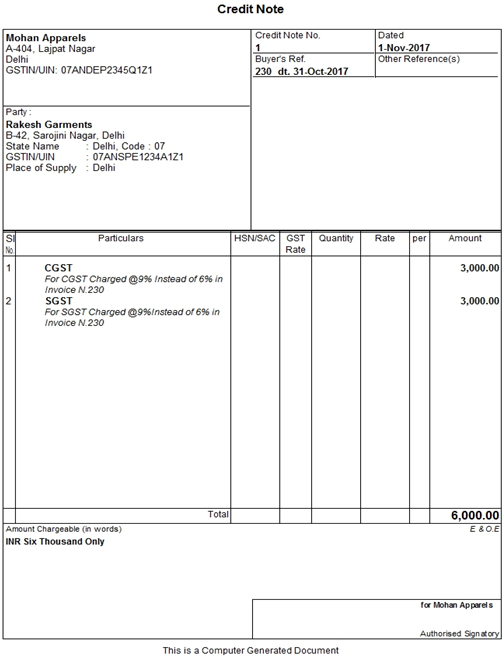

Example: On 2nd Feb, '18, Johan & Co., a registrant in Mumbai, supplies 10 Monitors @ 10,000 each, to Noon Electronics, a registrant in Mumbai. 18% GST charged on the supply is 1,800. On the same day, Noor Electronics returns 1 monitor to Johan & Co., as it was found to be damaged in transit. In this case, Johan & Co should issue a credit note to Noon Electronics for the monitor returned and reverse the GST charged on the monitor. The Tax Credit Note to be issued by Johan & Co. is shown below.

Example -2 of Credit Note

When cash discount is allowed at the time of collecting payment from a customer in terms of an agreement entered into prior to the supply, then the supplier would issue a credit note to the customer to the extent of such cash discount, to declare that he ‘OWES’ money.

Then, the original amount due to MINUS the credit note is the revised value of supply that the customer pays the supplier. To this extent, the GST thereon would also stand reduced, subject to conditions.

Conditions which must be satisfied for issuance of credit note in GST

The conditions applicable on an issue of credit note in GST are listed below:

- The supplier issues the credit note in respect of a tax invoice which has been issued by him earlier.

- The credit note cannot be issued any time after either of the following 2 events (“due date for credit note”):

|

Event 1 |

Annual return has been filed for the FY in which the original tax invoice was issued; or |

|

Event 2 |

September of the financial year immediately succeeding the financial year in which the original tax invoice was issued. (i.e., for a tax invoice issued in April 2018, as well as a tax invoice issued in March 2019, the relevant credit notes cannot be issued after September 2019); |

- The credit note so issued must be declared in the returns for the month in which they are issued, by the supplier and also the recipient, and latest by the due date for a credit note as specified above.

- The recipient, on declaring the same, must claim a reduction in his input tax credit if the same had been availed against the original tax invoice.

- A credit note cannot be issued if the incidence of tax and interest on such supply has been passed by him to any other person.

- You can issue a consolidated credit note against multiple tax invoices. The earlier provisions of issuance of a credit note against single invoice and linking the same have been removed.

- In case of a credit note issued for a discount, the discount must be provided in terms of an agreement entered into before or at the time of supply, as provided under the Act.

- The credit note contains all the applicable particulars as specified in CGST Rules, 2017.

Credit Note Format in GST

The debit and credit note in GST shall contain the following details :

- name, address, and GSTIN of the supplier

- nature of the document.

- a consecutive serial number containing only alphabets and/or numerals, unique for a financial year.

- date of issue of the document.

- name, address and GSTIN/ Unique ID Number, if registered, of the recipient.

- name and address of the recipient and the address of delivery, along with the name of State and its code, if such recipient is unregistered.

- serial number and date of the corresponding tax invoice or, as the case may be, bill of supply

- the taxable value of goods or services, rate of tax and the amount of the tax credited or, as the case may be, debited to the recipient.

- a signature or digital signature of the supplier or his authorized representative.

GST Credit Note Format

Impact of credit note in GSTR-3B and GST-1 monthly returns

GST Credit Notes in GSTR 1 Return

The supplier shall mention the details GST credit note in form GSTR-1. The details of the GST Credit Note should be mentioned in table 9B. The GST Credit Note details need to be mentioned separately for Registered and unregistered.

The following are details of GST Credit Note details issued registered business to be furnished in GSTR-1

- The Credit Notes (Registered) – Add Note page is displayed. In the Receiver GSTIN/UIN field, enter the GSTIN of the receiver (registered taxpayer) to whom the supply is made. Note: The Receiver Name field is auto-populated when the user enters the GSTIN of the Receiver

- In the Credit Note No. field, enter the credit note number or refund voucher number. Note: A Credit Note number should be unique for a given Financial Year (FY).

- In the Credit Note Date field, enter the date on which the credit note was issued. Note: The date should be before the end date of the tax period. Credit note date cannot be earlier than the original invoice date.

- In the Original Invoice Number field, enter the invoice number of the earlier-filed invoice (original invoice) on which the Credit Note is being issued or the number of advance receipts against which the refund voucher is issued.

- In the Original Invoice Date field, enter the original invoice date.

- From the Note Type drop-down list, select whether the details added are for a Credit Note or refund voucher.

- In the Note Value field, enter the value of the note or refund voucher.

- From the Supply Type drop-down list, select whether the note or voucher is added for an invoice of Inter-state or Intra-state transaction.

- Select the checkbox provided Is the supply eligible to be taxed at a differential percentage (%) of the existing rate of tax, as notified by the Government in case supply is eligible to be taxed at a differential percentage of the existing rate of tax.

In the case of Intra-State transaction:

In case the POS (place of supply) of the goods/ services is the same state as that of the supplier, the transaction is an Intra-State transaction. Notice, fields for Central Tax and State/UT Tax appear.

- In the Taxable Value field against the rates, enter the taxable value of the goods or services.

- In the Cess field, enter the cess amount.

Note: The Amount in Tax fields are auto-populated based on the values entered in Taxable Value fields respectively. However, the taxpayer can edit the tax amount. The CESS field is not auto-populated and has to be entered by the taxpayer.

GST Credit note in GSTR 3b

In GSTR 3B we don’t have a separate tile for disclosing the details of a credit note issued. Instead, it is dealt as a tax adjustment by way of deduction from Total taxable value and tax liability and only the net tax receipts are recorded in the tile ‘Details of outward supplies and inward supplies liable to reverse charge'.

Latest Blogs

Nuts & Bolts of Tally Filesystem: RangeTree

A Comprehensive Guide to UDYAM Payment Rules

UDYAM MSME Registration: Financial Boon for Small Businesses

Understanding UDYAM Registration: A Comprehensive Guide

MSME Payment Rule Changes from 1st April 2024: A Quick Guide

Are Your Suppliers Registered Under MSME (UDYAM)?